CapMan is an investment company. The vision is to be a long-term owner and create added value for the shareholders in the long term. CapMan mainly invests in medium-sized unlisted companies, properties and infrastructure facilities around the Nordic market. Furthermore, the company offers asset management, purchasing activities as well as analysis, reporting and back office services. CapMan was founded in 1989 and its headquarters are in Helsinki, Finland.

Regnskabsmeddelelsen for 4. kvartal lå under vores forventninger på grund af omkostninger og investeringsafkast. Der var dog ingen overraskelser i udsigterne, og 2026 bliver et helt afgørende år for selskabets investeringscase.

For asset managers on Nasdaq Helsinki, the trend has been mixed. The market situation has been very challenging for operators focusing on alternative investments, particularly real estate, while traditional asset management has continued to grow strongly.

For financial companies, 2025 has been very positive in terms of the operating environment, with strong capital market development and stabilized interest rates. However, the performance of the companies has been varying, and many companies we follow have suffered particularly from the subdued development of alternative investment returns (new sales and performance fees).

Overall, the Q3 report was good and in line with our expectations. New sales are still cumbersome, but there is finally light at the end of the tunnel for the market. Our forecasts still expect significant earnings growth, and this is subject to success in new sales.

CapMan released slightly better-than-expected Q3 results this morning. The earnings were in line with expectations, and the important management fees grew slightly more than we expected.

We expect the company to post good earnings in a seasonally strong quarter. However, fundraising remains gloomy, and the fundraising outlook is by far the most important aspect of the report.

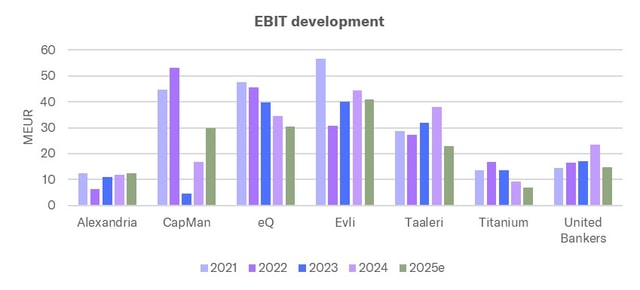

In this article, we review the quality of earnings of listed asset managers. In summary, the quality of earnings varies significantly within the sector, but on average, the level is quite good. The level has also improved in recent years, as the share of recurring fees has increased. We note that we have made the comparison at the group level, and thus the comparison does not account for the companies' differing business structures. We excluded Aktia from our review as the necessary information on its asset management is not available.

Asset managers' results declined sharply during the first half of the year. However, underlying factors include challenges in the real estate market and a decline in performance fees, and the operational development shown below has been largely positive. The outlook for the sector is positive, and as long as geopolitical risks remain in the background, companies in the sector are poised for robust earnings growth in the second half of the year.

The Q2 report did not offer any major surprises, and the clear earnings miss was entirely attributable to investment portfolio returns. We have not made changes to our forecasts and expect a significant earnings improvement in the coming years. For bottom-line growth to materialize, successful new sales are required, and the company has a clear opportunity to demonstrate this during the rest of the year.

The early part of the year has been moderate for asset management companies. Although stock prices are near their all-time highs in many places and interest rates have been in clear decline, market sentiment has been cautious, especially due to geopolitical tensions. Companies in the sector describe the early-year sentiment as mostly expectant. At the same time, however, the general tone of the comments has been cautiously positive.

CapMan announced yesterday that it has acquired a majority stake in the German-based real estate debt specialist CAERUS Debt Investments AG At the same time, CapMan will launch a new investment area “Real Asset Debt” Although the transaction is relatively small for CapMan (earnings impact of a few percent), the acquisition is clearly strategic, as it provides CapMan with access to a new asset class and market.

CapMan's Q1 report was ultimately quite neutral. The market situation will continue to hamper new sales in the short term, but the strong earnings growth outlook for the next few years remains intact. Once earnings growth is realized, the stock will be cheap, but due to the uncertainty surrounding the realization of new sales, we are holding back on a stronger view for the time being. We reiterate our EUR 2.1 target price and Accumulate recommendation.